The office rental market in Singapore experienced a slight dip in 3Q2024, following a strong rebound in the previous quarter. The URA office rental index (Central Region) increased by 3.1% in 2Q2024 but saw a 0.5% decline this quarter, reflecting ongoing rental volatility since 1Q2024, says CBRE.

The dip in rent has resulted in a smaller year-to-date increase in office rents, which now stands at 0.8% for the period from 1Q to 3Q2024, down from 1.3% the previous quarter. "The prime CBD office space, particularly Category 1 office buildings, showed signs of weakness," says Tricia Song, CBRE head of research for Southeast Asia.

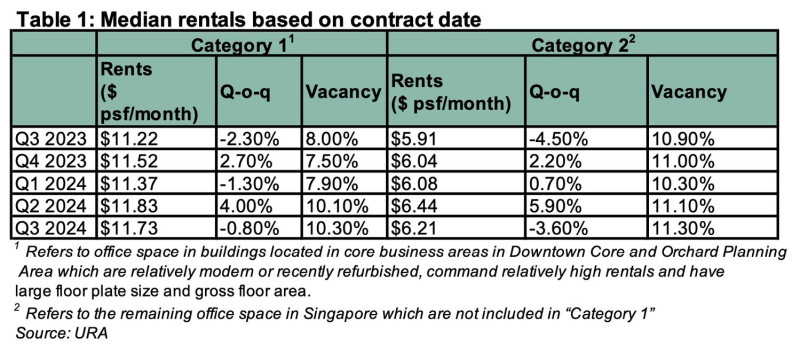

Based on contracts signed, median rents declined by 0.8% q-o-q in 3Q2024 after a significant 4.0% increase in 2Q2024.

Read also: Metro and Sim Lian JV to acquire Sydney office building for A$196.4 mil

Advertisement

Advertisement

CBRE Research attributes the softness to a recent surge in supply, notably the completion of IOI Central Boulevard Towers, which added 1.2 million sq ft of prime office space in the CBD. Consequently, Category 1 office vacancy rose to 10.3% in 3Q2024, up from 7.5% at the end of 2023.

Shadow stock in the CBD Grade A office space remains low, at pre-pandemic levels of about 0.2 million sq ft in 3Q2024, notes Cushman & Wakefield (C&W). It is down from the previous peak of 0.3 million sq ft in 2Q2023.

According to CBRE’s Song, lease renewals have primarily driven the office market as occupiers adopt a cost-conscious approach amid high interest rates and a capital-intensive environment. However, she adds that there has also been an increase in relocation activities.

Landlords prioritising occupancy over market-leading rents

Some landlords facing larger volumes of available space have prioritised occupancy over securing market-leading rents, adds Song, contributing to the decline in overall rents for 3Q2024.

"Despite these trends, the office sector remains distinctly two-tiered," says Song. "Competition for premium spaces in the best buildings remains strong, particularly for high floors with unobstructed views and lift lobby frontage. In such cases, tenants are willing to pay a premium over and above the typical Grade A average rent."

CBRE notes a significant trend of businesses in the legal, emerging tech, and professional services sectors relocating to high-quality buildings in prime city centre locations. "Occupiers are adopting a cost-conscious approach amid high interest rates and a capital-intensive environment," says Song.

Read also: Rents of prime office space in Singapore 21% higher than wider Grade-A stock: Savills

Advertisement

Advertisement

However, there has also been an increase in relocation activities. Some landlords, facing larger volumes of available space, are prioritising occupancy over securing market-leading rents, contributing to the decline in overall rents for 3Q2024, notes CBRE.

"The office market continues to see some degree of right-sizing as companies adjust their real estate footprint," says Wong Xian Yang, head of research for Singapore and SEA, Cushman & Wakefield (C&W). Some have reduced their spatial requirements, while others have moved to better quality and located offices.

Net demand turned negative

Central Region office net demand turned negative, dropping 0.2 million sq ft in the first three quarters of 2024, reversing the positive 0.6 million sq ft over the same period last year. Nonetheless, net demand in the Downtown Core remained positive at 0.5 million sq ft. However, this is about half of the one million sq ft registered over the same period last year.

Office demand has been skewed towards smaller users given the absence of large occupiers and large leasing deals owing to constraints in capital expenditure, says Wong. "Landlords are increasingly looking to offer fitted-out solutions to increase the marketability of their vacant office spaces."

"The rise in secondary office space has created opportunities for occupiers on the flight to quality," says Wong. He adds that much of the space previously occupied by Meta at

South Beach Tower has already been taken up or is in advanced negotiations by new and existing tenants.

The market is still going through a relatively soft patch amid still-elevated interest rates, says C&W’s Wong. However, there are several catalysts on the horizon that could escalate demand and rental growth. Most landlords are expected to hold on to their asking rents, he adds, with most Grade A offices remaining well-occupied. For 2024, CBD Grade A office rents are expected to grow 1% to 2% y-o-y.

Read also: Project Spotlight: This Bishan condo has over 700 profitable transactions

Advertisement

Advertisement

Central office prices up 0.6% in 3Q2024

"Office leasing activity may pick up towards 2025, fuelled by interest from emerging tech industries, wealth management firms and professional services companies," says Wong.

Demand for offices in the Central Region is expected to be supported by a tight labour market and high office attendance, driven by return-to-office solid mandates.

Furthermore, the postponement of Shaw Tower's completion from 2025 to 2026 will tighten the supply next year, with the only significant new supply expected to come from the completion of Keppel South Central (0.6 million sq ft).

With supply tightening and demand improving due to lower interest rates, Central Region office rents could be poised for more robust growth in 2025, says Wong. Occupiers should be ready to capitalise on opportunities before market optimism picks up.

In terms of pricing, Central Region office prices increased by 0.6% q-o-q in 3Q2024, marking the second consecutive quarter of growth. It was primarily driven by the 47% q-o-q rise in transaction volumes for strata offices in the Central Region, mainly due to the sale of office spaces at

Tong Building and Solitaire on Cecil.